How High-Income Earners Can Legally Reduce Taxes in California

California is legendary for its sunshine, but for high-income earners, it is equally known for its 13.3% top marginal tax rate—the highest in the United States. As we move into 2026, navigating the intersection of California’s progressive tax brackets and new federal provisions under the One Big Beautiful Bill (OBBBA) requires more than just basic filing; it requires a proactive, year-round strategy.

If you are a business owner, executive, or high-net-worth individual, "tax season" shouldn't be a post-mortem of what you owe. It should be the final step in a legal reduction plan. Below are the most effective strategies to lower your California tax burden this year.

1. The Pass-Through Entity (PTE) Tax Election

For business owners, the PTE Tax remains the single most powerful "SALT workaround" in California. Under Senate Bill 132, California has extended this election through 2030.

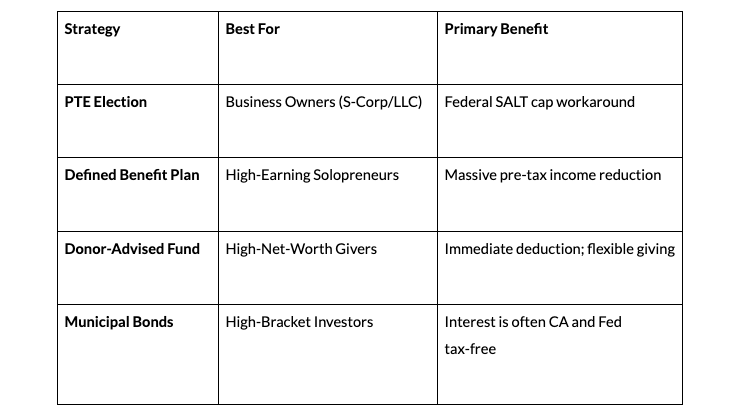

How it works: Eligible entities (S-Corps, Partnerships, and LLCs treated as partnerships) can elect to pay a 9.3% tax at the entity level on qualified net income.

The Benefit: This tax is fully deductible on your federal return, bypassing the federal $10,000 (or $40,000 for 2026) State and Local Tax (SALT) deduction cap.

2026 Update: Previously, missing the June 15 prepayment deadline resulted in automatic disqualification. Starting in 2026, you can still elect into the PTE even if you miss the deadline, though your credit will be reduced by 12.5% of the underpayment.

2. Leverage California’s Progressive Tax Brackets

California uses a progressive system with nine brackets ranging from 1% to 12.3%, plus a 1% Mental Health Services Act tax on taxable income exceeding $1 million.

For tax year 2026, the top 12.3% rate applies to single filers with income over $742,954 and joint filers over $1,485,907 (FTB 2026 Rates). By shifting income into lower-earning years or deferring bonuses through Non-Qualified Deferred Compensation (NQDC) plans, executives can keep more of their earnings out of that top 13.3% "danger zone."

3. Advanced Charitable Giving: Donor-Advised Funds (DAF)

Writing a check to a charity is the most common way to give, but for high-income earners, it is often the least tax-efficient.

Bunching Strategy: Under the OBBBA, the standard deduction for 2026 is $16,100 for singles and $32,200 for joint filers. If your annual giving doesn't exceed these amounts, you get no extra tax benefit. By "bunching" three years of giving into one year via a DAF, you can far exceed the standard deduction threshold and maximize your itemized savings in a high-income year.

Appreciated Securities: Donating stock that has grown in value allows you to claim a deduction for the full fair market value while avoiding the capital gains tax you would have paid if you sold the asset first.

4. Strategic Retirement Contributions & "Super Catch-Ups"

Maximizing pre-tax contributions is the foundation of tax reduction. For 2026, the contribution limits have increased:

401(k) / 403(b): $24,500.

Catch-up (Age 50+): $8,000.

Super Catch-up (Age 60–63): $11,250.

For business owners, establishing a Defined Benefit Plan can allow for contributions exceeding $100,000–$200,000 annually, depending on age and income, providing a massive dollar-for-dollar reduction in taxable income.

Comparison of Primary Tax Reduction Tools

5. Tax-Loss Harvesting and Asset Location

It is not about what you earn; it is about what you keep after Uncle Sam and the Franchise Tax Board (FTB) take their share.

Harvesting: Use market volatility to sell "losing" positions to offset capital gains. If your losses exceed your gains, you can use up to $3,000 to offset ordinary income and carry the rest forward.

Location: Keep tax-inefficient assets (like high-dividend stocks) in tax-deferred accounts (401k/IRA) and hold tax-efficient assets (like index funds or Municipal Bonds) in taxable brokerage accounts.

Protect Your Wealth with Precision

California’s tax code is dense, and with the potential for new measures like the 2026 Billionaire Tax Act looming on the ballot, high-income earners cannot afford to be passive. Legal tax reduction is a matter of structure and timing, not loopholes.